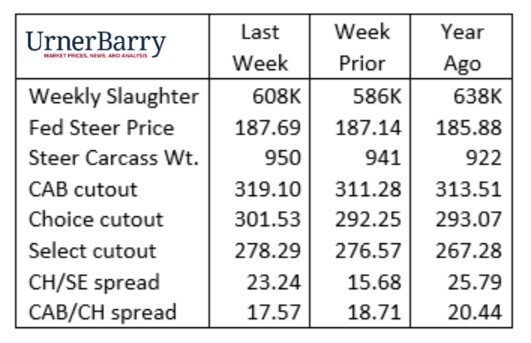

Federally inspected cattle harvest has been variable in the month of October. Specific to fed cattle, the month started strong with a 498,000 weekly total. The second week was a major pullback totaling just 468,000 head and recovering half of that large decline a week ago to average 489,000 head harvested.

Although packers chose to tighten product flow, fed cattle prices have plotted a higher trend, building from the mid-September $182-$184/cwt. range to last week’s average of $187/cwt. The October price trend has noted a price rally in the past three years. The price rally was followed by further November increases in 2021 and 2022 while last year’s October rally marked the top of the fed cattle market. The collapse in the November 2023 market was much less due to fundamentals and highly influenced by speculative futures activity.

Current market enthusiasm on the production side of the beef supply chain has swelled from the eruption of sharply higher carcass cutout values. Using the Choice 600-900 lb. carcass as the benchmark, that cutout price has increased $22.69/cwt. from October 1 through Monday this week. The production decline two weeks ago spurred prices higher, while the October seasonal trend calls for cutout values to begin their fourth quarter rally by mid-month. The price uptick has been steep, and it arrived earlier than typical this October.

The Certified Angus Beef ® brand cutout has, unsurprisingly, followed a similar uptick with weekly reports indicating a $20/cwt. increase through Thursday last week, with more upside yet to be charted through the current period. The onset of middle-meat demand is especially intense in this period and widening price spreads for carcass quality are once again appearing. However, the CAB cutout remains narrower than a year ago as record carcass weights, combined with exceptional marbling achievement, have boosted the brand’s supply. Over-supply is not a threat as the seasonal dip in industry average grading tends to mark the annual low in November.

October and December 2024 Live Cattle futures prices have posted an extended upward run since mid-September as futures have caught up to the weekly spot market. In the past week, those contracts have corrected slightly lower but are seeking to maintain a level par with cash cattle.

Ribeye Size Becomes a Factor

In the CAB Insider, we recently focused on the top five reasons eligible carcasses fail to meet all 10 of the brand’s carcass specifications. From our 2023 data set, carcasses with marbling scores below Modest 00 or “Premium Choice” captured 83% of carcasses that missed the mark. However, as carcass weights continue to balloon this fall, attention turns to the second-most commonly missed specification: the brand’s 10 to 16-inch allowable ribeye area requirement.

Intuition suggests that since hot carcass weight is also a brand specification, with a 1,100 lb. maximum, record-heavy carcasses could have the highest potential to miss brand acceptance.

While carcass weight and ribeye size aren’t directly correlated, heavier carcass weights are associated with larger average ribeye area. Research done more than a decade ago shows that ribeye growth tends to continue, but at a decreasing rate, as live weight passes 1,400 lb. or so, in steers. Inclusion of a beta-agonist in many modern steer diets is also a likely factor in increasing lean muscle growth at the end of the period, increasing ribeye area measurements upon harvest. But lean growth in the final days of the feeding period allowing heavier out-weights to be achieved is an economic benefit.

Without belaboring the topic, it’s appropriate to point out that feedyard management will follow where the highest returns exist. Currently adding more pounds to cattle already on inventory is the best proposition in the market.

We anticipate the traditional annual heaviest carcass weights by mid-November. Throughout this period Certified Angus Beef® brand carcass acceptance rate typically charts a lower seasonal trend due to declining quality grade. This November will feature a larger-than-normal slippage of brand-eligible carcasses due to ribeye size. This occurs as average steer carcass weights continually increase, and they were averaging 950 lb. two weeks ago.

Feeders will continue to reap rewards in the cost and return equation in a market that has recently moved to higher prices. Grid-sold cattle are, on average, capturing Choice and Prime quality premiums at a higher percentage rate this fall. Yet, yield grade and heavy-weight discounts threaten to devalue premiums for the heavy pens of steers, in addition to fewer CAB qualifiers.

Key Takeaways

Cattle Harvest Variability: October’s federally inspected cattle harvest has fluctuated, starting strong but experiencing a pullback. The average weekly harvest settled around 489,000 head after a dip.

Fed Cattle Prices: Despite tighter product flow from packers, fed cattle prices have risen, reaching an average of $187/cwt in October, marking a price rally similar to trends seen in previous years.

Carcass Cutout Values: There has been a significant increase in carcass cutout values, with a rise of $22.69/cwt since October 1st. This upward trend is typical for this time of year and is driven by production declines and seasonal demand.

CAB Brand Cutout Increase: The Certified Angus Beef (CAB) cutout also saw a $20/cwt increase, with expectations of further growth due to intense middle-meat demand, although the cutout remains narrower compared to last year.

Ribeye Size and Carcass Acceptance: A focus on ribeye size is crucial, as many carcasses fail to meet CAB specifications due to marbling issues and ribeye area requirements. As carcass weights increase, the likelihood of missing specifications also rises.

Market Dynamics: Heavier carcass weights may lead to higher returns for feedlot operators, with grid-sold cattle capturing higher quality premiums. However, yield grade and heavy-weight discounts could diminish these premiums.

###

Paul Dykstra-Certified Angus Beef/Northern Ag Network